Financial Happenings Blog

Thursday, May 26 2011

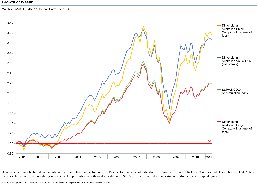

We have updated the Dimensional Fund Performance Graphs page. The page includes periodic performance data, growth of wealth graphs and average performance bar charts for the previous 1 month, 3 months, 6 months, 1 year, 3 years, 5 years and 10 years.

Commentary:

The graphs show a negative month of returns for all asset classes with all of the risk premiums under-performing the large company benchmarks.

Over the long run, however, the data continues to clearly show the existence of the risk premiums (small, value and emerging markets) that the research tells us should exist:

Australian Share Trusts - 10 Year returns

|

|

10 Yr Return

to April 2011

|

Premium over ASX 200

Accumulation Index

|

|

ASX 200 Accumulation Index

|

8.20%

|

-

|

|

Dimensional Aust Value Trust

|

11.82%

|

3.62%

|

|

Dimensional Aust Small Company Trust

|

12.15%

|

3.95%

|

International Share Trusts - 10 Year returns

|

|

10 Yr Return

to April 2011

|

Premium over MSCI World (ex Aust) Index

|

|

MSCI World (ex Aust) Index

|

-3.52%

|

-

|

|

Dimensional Global Value Trust

|

-0.97%

|

2.55%

|

|

Dimensional Global Small Company Trust

|

1.95%

|

5.47%

|

|

Dimensional Emerging Markets Trust

|

7.95%

|

11.47%

|

NB - These numbers are annualised returns for the 10 year period.

Regards,

Scott Keefer

Thursday, May 26 2011

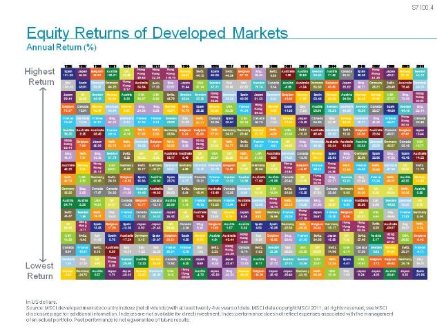

The following table provides a really interesting way to look at year by year returns for 18 of the major developed equity markets in the world over the past 25 years.

Please click on the above image to view a full page printable pdf

Adobe Reader® required Adobe Reader® required

download at Adobe.com

The take away is the great fluctuation in performance from year to year. Australia has had very strong years such as 2001, 2002 and 2009 but years like 2008 remind that only investing here is by no means a sure bet to better investments held in other nations. Another reminder of the importance of diversification

Thursday, May 26 2011

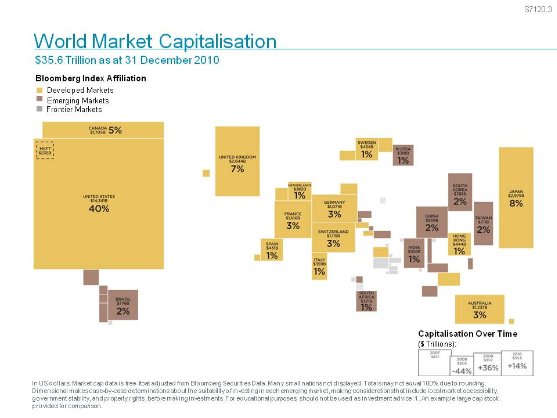

Today we have uploaded a great chart looking at the market capitalisations of major world markets in terms of US dollars as at the end of December 2010.

The chart shows that Australia was only 3% of the entire world market. Some might ask why then do we suggest that Australian shares make up 50% or more of recommended growth asset allocations? Our investment philosophy takes into account research suggesting that the franking credit benefits offered by Australian shares are not fully reflected into the value of Australian shares as they are not available to non-residents. This suggests that over the long term there is an extra benefit from holding Australia shares for residents of Australia. However we also acknowledge that including international shares provides diversification benefits for a portfolio.

Please click on the chart to view a full page printable pdf copy of the chart.

Adobe Reader® required

download at Adobe.com

Thursday, May 26 2011

The end of the financial year is an ideal time to consider your financial structuring for the year ahead. However if you have not yet put plans in place for this financial year it is not too late to put them into action. Here are some strategies to consider and as always, please seek individual financial advice before taking any action.

- Making a personal contribution of up to $1,000 into super to receive the government co-contributions.

- Making non-concessional contributions into super to get these assets into a tax friendly environment

a. This can include an in specie transfer of assets if you use a fund that allows this

- Making a concessional contribution into super to reduce tax payable on income and get assets into a tax-friendly environment

- Making a contribution into your spouse’s super fund if they are a low income earner and by doing so receiving a tax offset whilst also getting assets into a tax friendly environment

- Bringing forward any relevant tax deductions

To find out more details please take a look at our page - End of Financial Year Strategies to Consider

Monday, May 23 2011

Scott Francis in his latest Eureka Report article looks at the hidden tax rise contained in the government's latest budget. He suggests that due to the phenomenon of bracket creep, the increase in average wages is providing the government about $3 billion in extra tax receipts.

Scott concludes that bracket creep is an important concept for taxpayers to understand; it sees them facing increasingly higher tax rates unless tax brackets change as incomes increase. The resulting increase in government revenue means neither side of politics has ever tried to fix the problem, which could be done by the relatively simple step of indexing tax thresholds to inflation or wage rises.

Take a look at Scott's article here - The tax rise no one noticed

Monday, May 23 2011

The Australian Bureau of Statistics is the official determiner of inflation in the economy. The calculation for their Consumer Price Index is based on the cost to purchase a basket of goods. This basket, including weightings, are currently as follows :

- Food (15.44%)

- Alcohol and tobacco (6.79%)

- Clothing and footwear (3.91%)

- Housing (19.53%)

- Household contents and services (9.61%)

- Health (4.70%)

- Transportation (13.11%)

- Communication (3.31%)

- Recreation (11.55%)

- Education (2.73%)

- Financial and insurance services (9.31%)

(NB - these allocations are soon to be adjusted in the June quarter calculations.)

One potential problem with the inflation calculations as they relate to retirees is whether the basket of goods is a fair representation of what people in retirement are purchasing. This is important because the latest publication issued in April suggests that prices for food, alcohol and tobacco, housing (including utilities), education and health have been the major contributors to inflation over the past year. Out of these I would suggest that retirees spend less on average for education but more on average for the other categories.

This would suggest that inflation has run at a higher rate than the 3.3% annual rate calculated by the ABS.

Today, The Association of Superannuation Funds of Australia have published their latest Retirement Standard report. This publication attempts to calculate what a modest or comfortable lifestyle would cost for singles or couples.

These calculations are also subject to the risk that the definition of what retirees are purchasing used in the study does not match the actual situation but I believe it probably provides a better reflection due to the more concentrated focus.

The latest figures relating to the period ending December 2010 suggest the following levels of income would be required in retirement:

Modest lifestyle - single - $21,218

Modest lifestyle - couple - $30,708

Comfortable lifestyle - single - $39,393

Comfortable lifestyle - couple - $53,879

For further details as to how these amounts are calculated please refer to ASFA's Retirement Standard - December 2010

Using these calculations compared to past calculations should give a clearer indication of inflation being experienced by retirees. According to the Retirement Standard figures for the 12 months to the end of December inflation has been:

Modest lifestyle - single - 6.11%

Modest lifestyle - couple - 9.36%

Comfortable lifestyle - single - 2.03%

Comfortable lifestyle - couple - 4.16%

The ABS official inflation figure for the same 12 month period was 2.7%.

The results from the ASFA Retirement Standard study are above the ABS data for all but singles looking for a comfortable lifestyle.

A word of caution, ASFA rejigged their definitions for determining calculations starting with the March 2010 study. Therefore we have not yet seen a full year with these new definitions and calculation methods. Not until the next publication will be able to be confident of what the data is telling us.

In a nutshell, it does appear plausible that inflation for retirees is running at a hotter pace than the ABS's official inflation figures might otherwise suggest. This is very important for those in and preparing for retirement as a clear understanding of the movement of prices will help inform what a sustainable level of draw down from investments and superannuation pensions will look like.

Regards,

Scott

Thursday, May 19 2011

Reports are being published today relating to a study conducted by an independent market research company commissioned by the Australian Securities & Investments Commission. ASIC commissioned the study to better understand the personal consequences of investors not being fully compensated and to help inform submissions to the government review into whether a statutory compensation scheme should be introduced in Australia.

The following is taken from Andrew Main's report in The Australian - Move to compensate investors for bad financial advice

Among key findings were that investors who suffered the most had invested all their money, had not diversified or went into debt as part of their investment strategy....

Most investors' losses were associated with an underlying product that was either frozen or collapsed, and the impact of the monetary loss was immediate on investors who did not have a financial buffer. For others, the first six months from when they discovered their loss were critical....

Every single investor in the worst affected category, which usually involved losing their house, reported serious illness following the financial loss.

The key point I took away from the reporting of this study was that the worst-affected investors covered by the new study were in the following types of scheme:

- inner city unit developments,

- mortgage investment schemes,

- rural managed investment schemes such as forestry or horticulture,

- structured investment such as hedge funds and infrastructure funds, and

- investors who geared up against their home equity and took out margin loans to invest in assets which lost value.

My heart goes out to those who have been hurt by dreadful financial advice and I hope that the government can implement a structure to support those who were mislead or deceived.

It is also important that we all learn from the terrible misfortune of others and make sure that we are careful to properly investigate investment options and seek a second or third opinion if there is any doubt.

At A Clear Direction you can be assured that none of these investment options are in our preferred investment portfolio structure.

Regards,

Scott

Thursday, May 19 2011

The end of financial year sees many of us looking at our taxable income to see how we can legitimately reduce the tax burden. There are a number of approaches recommended with some being totally acceptable where appropriate to your individual circumstances. The following ideas are common:

- salary sacrificing into super to reduce taxable income including capital gains

- prepaying investment loan interest payments

- making a superannuation contribution for a low income spouse

Another strategy that was more common before the GFC was to invest in agribusiness schemes which were provided friendly tax arrangements. Unfortunately many of these turned out to be poor investments and even though you could save some tax going in you lost a lot more through the failure or poor performance of the investment.

This is a key reminder for all of us that when searching for tax breaks it is crucial to weigh up the underlying investment first and then if this stacks up the tax break provides a bonus.

Unfortunately there are also promoters of a range of schemes that have gained the attention of the Australian Tax Office. The ATO have produced a handy guide - Understanding tax-effective investments - to assist tax payers determine whether a proposed approach will be allowed by the ATO. There are 16 categories mentioned including mortgage management plans, early access to super, scholarship trusts and a range of strategies around the use of trusts privately and in business.

The key message from the guide is to carefully check the credentials of the provider of the advice and seek independent guidance. The ATO suggests the alarm bells should be going off with arrangements that:

- Offer zero risk guarantees

- Do not have a prospectus or product disclosure statement

- Refer you to a specific adviser or expert

- Ask you to maintain secrecy to protect the arrangement from rival firms and discourage you from getting independent advice.

At this time of the year it is easy to rush into an arrangement that sounds brilliant and will relieve the tax burden in months ahead. If you stumble into an inappropriate scheme the penalties are great not least of which is having the attention of the ATO squarely focused on you. A circumstance that I am sure most of us would prefer not to have.

Regards,

Scott

Tuesday, May 17 2011

I like to keep abreast of a broad range of opinions and research relating to finances. One of these sources is the prestigious Stanford Graduate School of Business. A new piece of research out from Stanford suggests that time not money provides the greatest level of happiness. It might at first seem that this topic is unrelated to the financial planning process but digging deeper it actually defines the most important aspect of the relationship between a client and their adviser.

The authors, Jennifer Aaker and Melanie Rudd at Stanford University, and Cassie Mogilner at the University of Pennsylvania, published their findings in the Journal of Consumer Psychology this year - "If Money Doesn't Make You Happy, Consider Time". The conclusion from the report is that for greater levels of happiness we need to spend our time wisely and in particular:

- spend time with the right people

- spend time on the right activities

- enjoy experiences without spending time actually doing them

- expand our time

- be aware that happiness changes over time

None of this seems to be rocket science but as the report points out we struggle to sit back and reflect on these 5 key points and often rather get caught up in the pursuit of money and objects. If you are looking for a little more detail about the research it can be found here - If Money Doesn't Make You Happy, Consider Time.

How can a financial adviser help?

Financial advisers are not life coaches, although it feels like it sometimes, however a key aspect of the relationship with a financial adviser is the confidence and peace of mind that it should bring. We are here to at least help manage if not totally manage your financial affairs. This ticks both the goals of money and time. We should be working to ensure that you are smart with the money that you have but also by delegating some of the responsibilities to your financial adviser you are freeing up time both in physical terms but also the mental stress time that you need to exert thinking about your financial affairs.

This second aspect of the relationship is very difficult on which to place a value but for many it is well and truly the most valuable aspect of the relationship between adviser and client.

Regards,

Scott

Sunday, May 15 2011

A frequent point of discussion around investment circles is to consider the strength of national economies and make investment decisions based on the relative strength of these economic. i.e. invest more in economies with strong economic growth and less in those with lower levels of growth. If only it was that simple. Research on this topic shows that there is no clear correlation between per capita economic growth as measured by gross domestic product and share market returns. A study published in 2005 by Jay Ritter, Economic Growth and Equity Returns, showed that for 16 countries there was actually negative correlation - countries with above average growth provided below average share market returns.

Jim Davis from Dimensional in the USA has also produced his own analysis looking at Emerging Market economies. Larry Swedroe in his blog - Why Successful Economies Don't Mean Great Stock Returns - explains Jim's results:

Jim Davis chose to study the emerging markets because of the widely held perception is that the markets of the emerging countries are inefficient. At the beginning of each year, Davis divided the emerging market countries in the IFC Investable Universe database into two groups based on GDP growth for the upcoming year:

- The high-growth group consisted of the 50 percent of the countries with the highest real GDP growth for the year.

- The low-growth countries were the other half.

He then measured returns using two sets of country weights-aggregate free-float-adjusted market-cap weights and equal weights. Companies were market-cap weighted within countries. The results are shown in the table below.

The results show that there is very little difference in share market performance between high growth and low-growth countries.

Both studies suggest that economic growth potential was factored into the price of shares. This reminds us that it is events in the future which we really can only guess at, that will determine which markets perform better than others.

We in Australia all too well understand this outcome seeing the returns of the Australian share market over the past year providing disappointing results from what is widely referred to as one of the strongest developed market economies in the world. (NB - In US dollar terms the Australian share market has performed in line with but not significantly out-performed the world dominating, in terms of size, US market.)

So what should we take away from this?

These results suggest that investors should take care basing investment decisions on whether an economy has strong economic growth, rather we believe it is better to develop a wide diversification of investments across all the available world share markets.

Regards,

Scott

|

|

|

|